- 51% respondents anticipate increased costs if production shifts, raising financial concerns

- Container surplus, a by-product of supply chain chaos and excess capacity, adds complexity

- Container repositioning efficiency is the real issue, not geographical production

9 November 2023, Hamburg, Germany: The global shipping industry is currently grappling with a complex challenge that revolves around a crucial element – shipping containers. The real issue at hand is not the geographical concentration of container production but rather the efficient positioning of the global container pool.

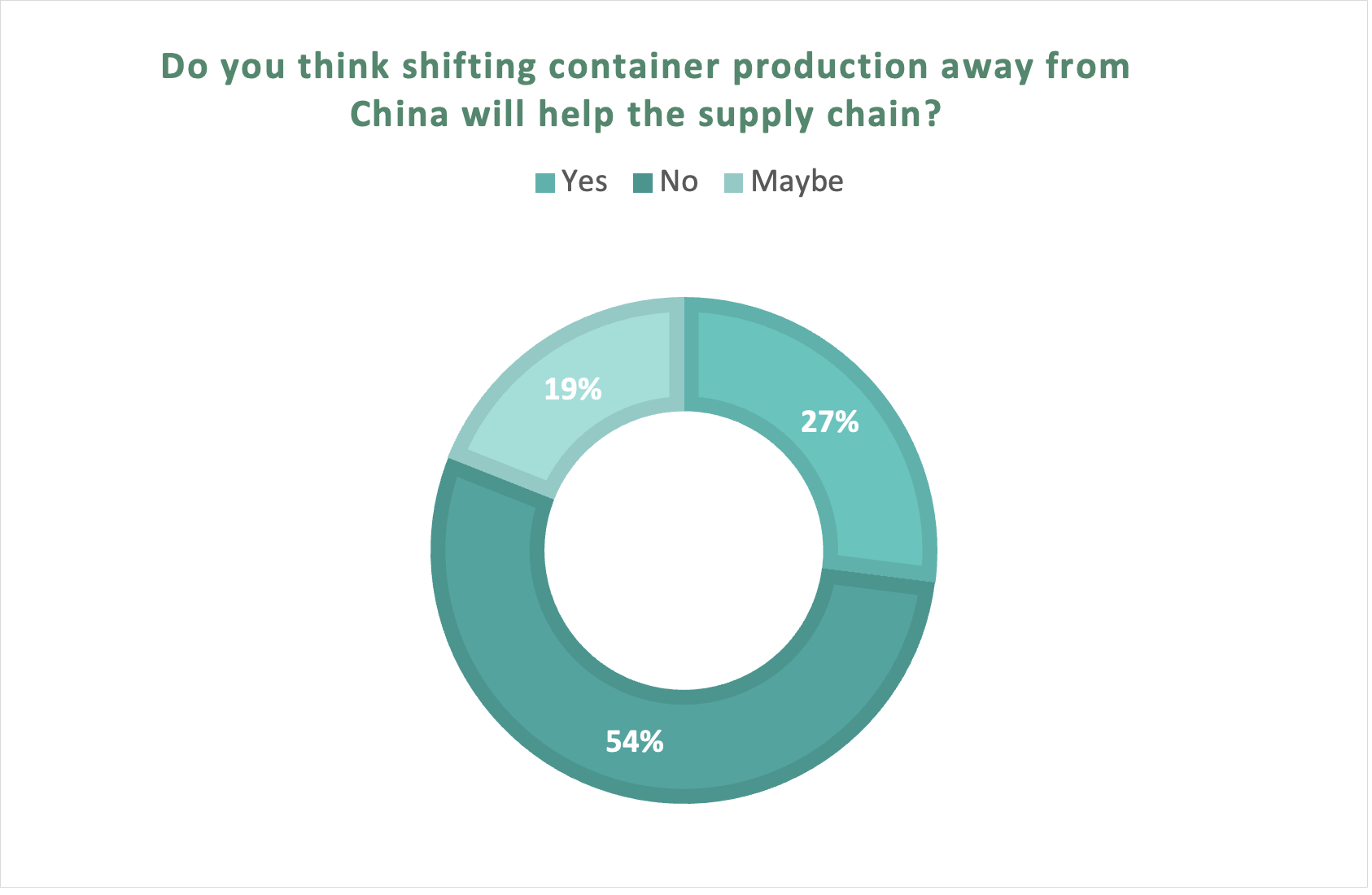

According to Container xChange’s recent survey, 54% of container logistics professionals did not believe that shifting container production away from China would improve the supply chain.

Container xChange surveyed around 1500 supply chain professionals to gauge container logistics and supply chain professionals’ sentiment around shifting container production away from China. The survey also delved into concerns about potential cost implications stemming from shifting container production. A significant 51% of respondents anticipated that such a transition could result in increased costs in the shipping industry, indicating a strong concern about the financial aspect of the change.

“In the global trade landscape, it’s not where containers are produced that matters but rather where they are repositioned at the right place and the right time. This challenge is further exacerbated by factors such as supply chain disruptions, labor strikes, COVID-19, and the unforgettable incident in the Suez Canal.” Added Christian Roeloffs, cofounder and CEO, Container xChange, an online global container logistics platform.

Recent years have seen a notable shift in container production, with countries like Vietnam and India aspiring to reduce reliance on China, the giant in container manufacturing.

The Challenge of Container Repositioning

A surplus of containers has become a growing concern. The container industry experienced a 13% boost in capacity in 2021 due to various supply chain issues, increasing transit times. However, the shorter transit times that followed and fluctuating demand left the industry with an excess of 13 million containers globally in the spring of 2023. To make things more complicated, this surplus has led to a drop in container rates, and there’s a cost attached to it – about $0.5 to $1 per TEU per day for regular containers, and potentially more for specialized containers like reefers and chemical tanks.

What’s even more telling is that data from Drewry shows that the production of 20-foot equivalent units (TEUs) plummeted by a staggering 71% from 1.06 million to 306,000 between the first quarter of 2022 and the same period in the following year. The push to diversify container production away from China doesn’t provide a clear picture of how much capacity will shift away from the Chinese giant.

“There was a significant discussion about container scarcity during the pandemic, but it had nothing to do with any geopolitical underlying reasons. The only reason, in my view, would be geopolitical risk management — i.e., you want to hedge yourself against a black swan event where trade relationships with China are sanctioned or the like.

The numbers don’t lie. While diversifying container production away from China might seem like a great idea, we need to tread carefully. The surplus of containers and the complexities of repositioning containers raise concerns about the effectiveness of this strategy in addressing global supply chain challenges.”, said Christian Roeloffs, Co-Founder and CEO, Container xChange.

China’s Iron Grip as Container Pool Surge to Unprecedented Levels

In recent years, there has been a significant shift in container production, with countries like Vietnam and India seeking to reduce their reliance on China, the dominant player in container manufacturing. To better understand this landscape, let’s delve into the numbers. In 2021, China produced a staggering 7.1 million twenty-foot equivalent units (TEUs), a substantial increase from the average annual production in the previous decade, which stood at just 2.6 million TEUs. This places China at the forefront of container production, contributing to more than 95% of the world’s containers.

China’s advantage doesn’t stop at scale; they have a bustling export market, ensuring immediate utilization of their containers. In contrast, containers produced outside China often face skepticism due to quality concerns and higher costs.

New Contenders

Vietnam has emerged as a strong contender in this shift, with the capacity to manufacture a significant chunk of the world’s steel boxes. India is also stepping up to the plate, looking to diversify the container production landscape. But there’s a catch.

Containers produced outside China often face scepticism due to concerns about their quality. These non-Chinese containers may also come with a higher price tag, primarily because they can’t leverage China’s massive scale to keep costs down. When we look at the cost, it’s quite a difference. An Indian container can cost around Rs 1.46 lakh per box, while a Chinese one is a lot cheaper, at just Rs 75,000 each.

Moreover, the immediate demand for containers in China, driven by a significant export volume, adds to its appeal. New build containers in China, especially when produced in large quantities, offer more attractive economies of scale compared to Vietnam and India. The industry’s skepticism about how this transition will unfold is grounded in these considerations.

While India and Vietnam do present certain advantages, such as the ability to produce smaller batches and customize containers, the extent to which production will shift to India and China remains uncertain.

In addition, China’s unique advantage, immediate domestic demand, is not something others can replicate. This means that containers produced in places like Vietnam and India may not find as many immediate takers.

While the idea of diversifying production sources is intriguing, it’s important to recognize the challenges involved.

The changing dynamics of container production are a crucial development in the shipping industry. The desire to reduce dependence on China is understandable, but it’s essential to weigh the pros and cons carefully. The industry must navigate the tricky waters of an oversupplied market and the intricacies of container repositioning.

The current market is flooded with an abundance of shipping containers, well-equipped to meet the short-term surge in demand. This presents a unique opportunity to address persistent issues that have plagued the shipping industry for years.

Now is the time to rectify problems such as the inefficiencies in repositioning containers, ensuring the quality and reliability of containers produced outside dominant markets, and the implementation of robust, localized supply chain strategies.

In the long run, as demand rebounds, countries must ensure their supply chain strategies are effective, localized, and responsive to the demand hotspots, rather than focusing solely on container production. Finding a balanced and sustainable path forward is essential for the future of global trade and logistics.