28.09.2023

As Russia grapples with the western sanctions one year after the invasion in Ukraine, China supports by bolstering bilateral trade between the two nations. Container xChange investigates the intricacies of the China-Russia trade and how it impacts the container logistics industry, now and in future.

China – Russia trade ties

“There is significant cargo movement from China into Russia but very scarce movement back to China from Russia. Containers are piling up in Russia which means that the secondhand container prices are very low in Russia. You see a 40ft high cube container being on sale in Moscow for less than $1,000, while in other parts of the world it is almost double or even more. This is significant and has tremendously detrimental impact on the business of container logistics because of the high imbalance of demand and supply of containers.” said Christian Roeloffs, cofounder and CEO, Container xChange.

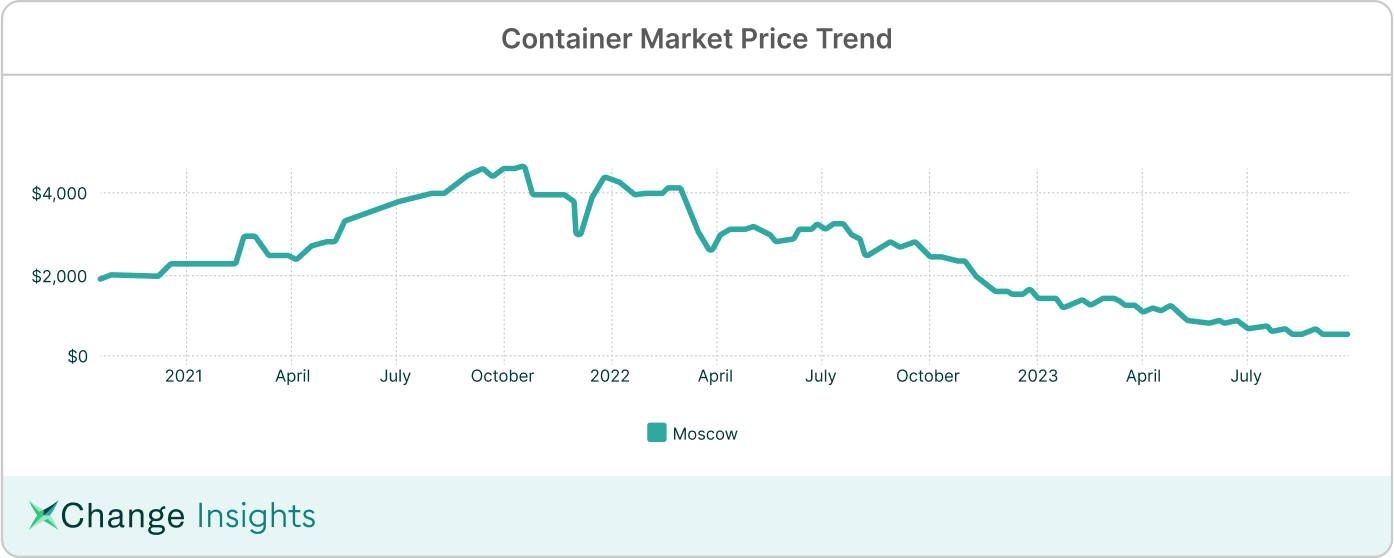

In February 2022, the average price of a 40ft high cube container in Moscow was $4,175, which is now $580 as of 25 September 2023. (See graph below)

Similarly, the average price of a cargo worthy 20 ft DC was $1,961 in February 2022, which has consistently declined and bottomed out to $675 as of 25 September 2023.

Similarly, the average price of a cargo worthy 20 ft DC was $1,961 in February 2022, which has consistently declined and bottomed out to $675 as of 25 September 2023.

“Currently there are around 150,000 surplus containers in Russia, and everybody is looking for an opportunity to return containers back to China. All containers from Russia to China go with a pickup charge. Regarding container trading, many Chinese companies are selling containers below market price to get rid of the boxes since it doesn’t make sense to send them back to China. From Moscow to Shanghai, the offline market offers around $1,500 for new containers. If cargo worthy containers are in good condition and cost less, they prefer to sell the boxes in the local market.

But this doesn’t mean that the market is bad. There are still many companies exporting as many as 4,000 SOC containers from Russia to China. The transactions between China and Russia are still very significant.” a customer of Container xChange shared.

China, traditionally a substantial purchaser of Russian energy, has now emerged as a vital source of imports, encompassing a wide range of products such as machinery, pharmaceuticals, auto parts, consumer goods, smartphones, cars, and agricultural equipment, from China. This shift has created a shortage of closed cargo containers, further intensifying the logistics challenge.

This shift is a direct result of numerous international companies exiting the Russian market amid ongoing geopolitical tensions and the conflict in Ukraine.

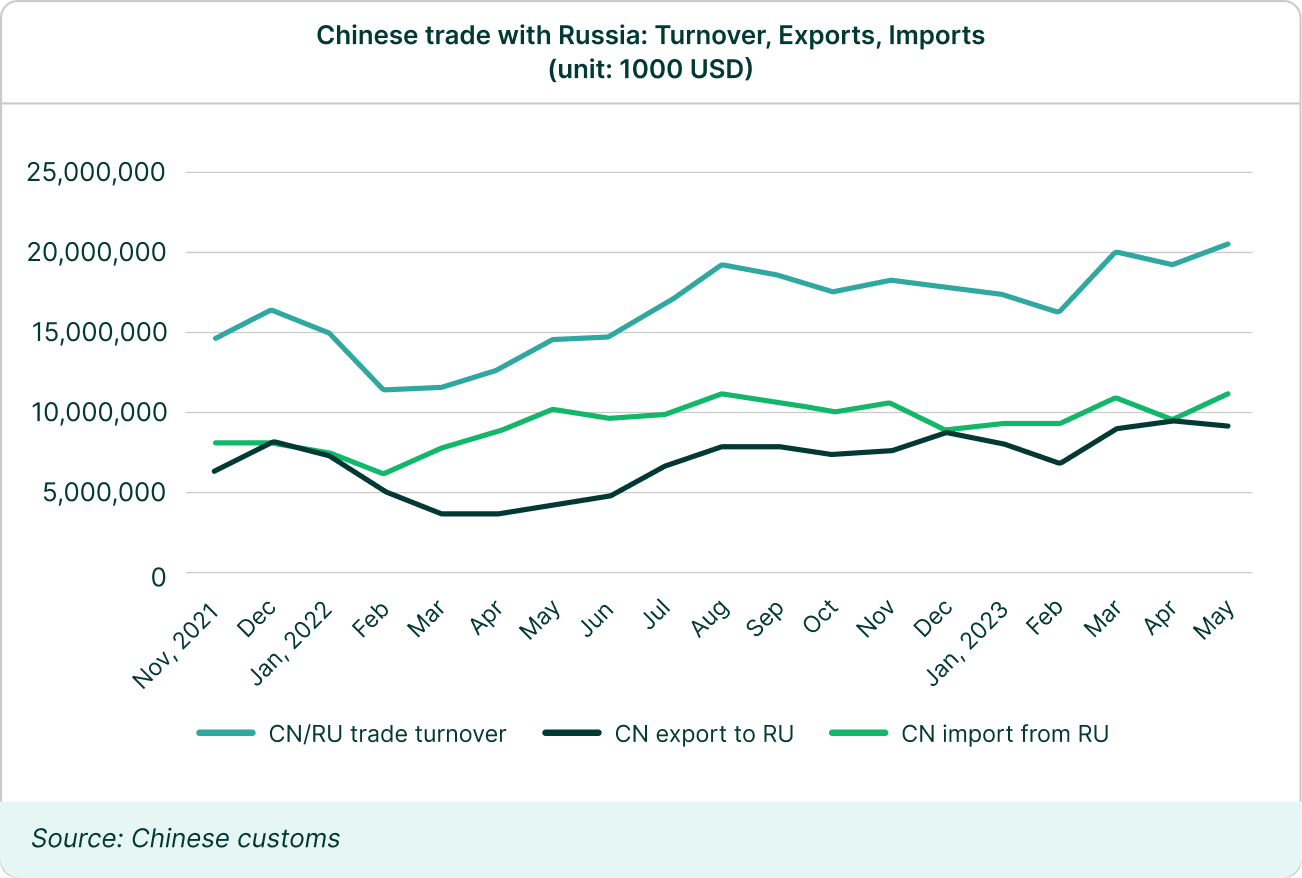

Trade between China and Russia witnessed substantial growth of 36.5% in the first seven months of 2023, totaling $134.1 billion, according to Chinese customs data. China’s exports to Russia surged by 73.4%, reaching approximately $62.54 billion, while imports from Russia also grew significantly by 15.1%, totaling $71.6 billion.

Soon after Russia’s invasion in Ukraine last year in February 2022, the bilateral trade between China and Russia dipped for a brief period of time and then picked up to reach record levels.

Russia anticipates that its trade volume with China will surpass $200 billion this year, a notable increase from the approximately $185 billion recorded in 2022.

Russia anticipates that its trade volume with China will surpass $200 billion this year, a notable increase from the approximately $185 billion recorded in 2022.

Surge In trade causing container imbalance

As imports from China to Russia continue to surge, it is leading to a significant trade imbalance and container congestion. According to a report from the VPost, Russian railway depots are grappling with an overwhelming accumulation of empty shipping containers originating from China. Managers at Russian shipping companies have expressed concerns about the severity of the situation, describing it as “almost critical” in regions like Moscow and central Russia.

This container crisis is primarily a consequence of the deepening trade imbalance between Russia and China. Russia is flooded with more containers carrying goods from China than it can dispatch back. Furthermore, the commodities exchanged between the two countries play a role in exacerbating the problem, as Russian raw materials are primarily transported to China via rail tanks and open wagons rather than in containers.

In an attempt to improve the container congestion, Russian shipping companies have started offering discounts to expedite the return of containers to China.

Overloaded Russian ports and roads are causing transportation inefficiencies. Although some investments have been made to improve infrastructure, fiscal constraints and the use of the National Wealth Fund to cover budget shortfalls complicate matters. Russia seeks Chinese investors to address these issues, but uncertainty stays due to recent actions against Western companies. However, Russia’s pivot to Asia hinges on substantial infrastructure development.

China-Russia trade: Current trends and prospects

As we look ahead to the future of China-Russia trade, it becomes evident that despite recent declines in shipping rates, operators providing container shipping services are pressing forward with their expansion plans on this trade lane.

One noteworthy development is the entry of CStar Line, a newcomer in the industry, into the China-Russia trade arena. In a parallel development, Yangpu New New Shipping has expanded its Northern Sea Route service, connecting China to St. Petersburg. This expansion follows the successful eastbound trial voyage by the 1,638 TEU Newnew Polar Bear, which departed from Xingang in August.

Despite recent rate declines in shipping to Russia, operators like CStar Line and Yangpu New New Shipping are finding profitability, especially during the summer peak season. Notably, cargo volumes from Busan to Russia’s Pacific ports saw a robust 6% increase in July, reaching 13,600 TEU compared to the previous month. However, the market faces pressure from new Chinese entrants, leading to a month-on-month decrease in the average freight rate for the Busan-Far East Russia route, ranging from $1,000 to $2,200 per TEU—a drop of approximately $100. These developments underscore the shipping industry’s resilience and adaptability as the China-Russia trade landscape continues to evolve.

Additional Data:

Strengthening trade Ties with Central Asian nations

In 2022, trade between Russia and Central Asian countries increased by 15%, reaching more than $42 billion. This growth is attributed to strong trade partnerships among countries in organizations like the Shanghai Cooperation Organization (SCO), BRICS, and the Eurasian Economic Union (EAEU). Central Asian nations, such as Kazakhstan, Kyrgyzstan, Tajikistan, Turkmenistan, and Uzbekistan, collaborate closely with Russia on technology and independence-related matters. This expansion of trade bolsters Russia’s regional influence and strengthens its ties with Central Asian partners.

The compatibility between Russia and China’s foreign policy objectives, emphasizing multipolarity and resisting control, may strengthen their partnership in Asia, impacting the region’s geopolitics. This shift towards Asia represents a clear trend for Russia towards establishing better trade partnerships with Asian countries.

Russia’s European trade challenges

Russia, a key euro area trade partner, experienced a 50% dip in trade with the region. While euro area exports to Russia initially dropped quickly, they have since partially recovered for non-sanctioned goods, while sanctioned goods exports remain low. Russia also reduced natural gas flows to Europe, causing a 90% drop in gas imports. Europe compensated by importing gas from Norway, Algeria, and Azerbaijan while increasing liquefied natural gas (LNG) imports, substantially diminishing Russia’s influence in European energy markets.

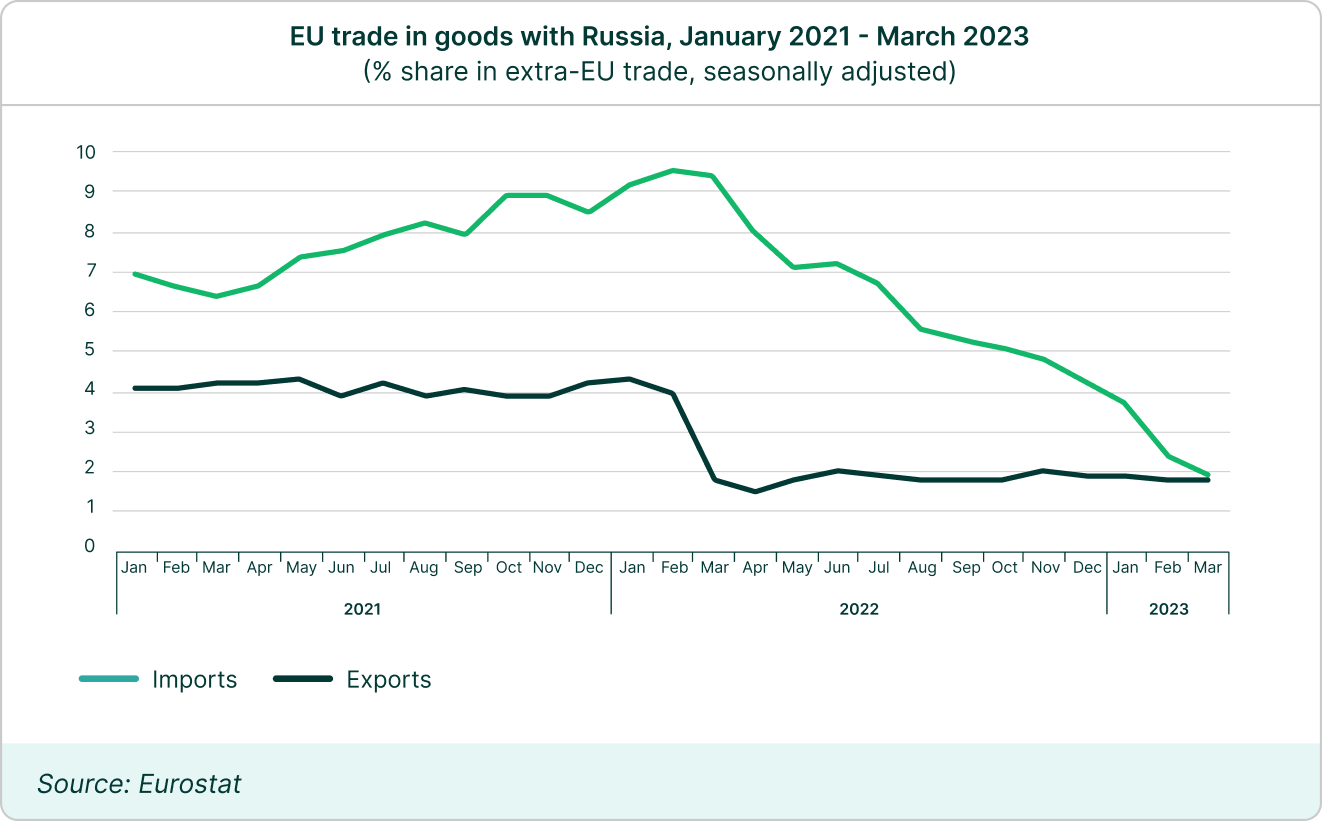

EU trade with Russia has been strongly affected by import and export restrictions imposed by the EU following Russia’s invasion of Ukraine.

Both exports and imports have dropped considerably below the level prior to the invasion. Seasonally adjusted values show that Russia’s share in extra-EU imports fell from 9.6% in February 2022 to 1.7% in June 2023, while the share of extra-EU exports fell from 3.8 % to 1.4% in the same period.

European sanctions and voluntary boycotts have redirected Russian trade away from the euro area, increasing dependence on non-sanctioning partners and leading to discounted commodity exports. This shift has reoriented Russia’s global trade, making it heavily reliant on China and other Asian countries.

European sanctions and voluntary boycotts have redirected Russian trade away from the euro area, increasing dependence on non-sanctioning partners and leading to discounted commodity exports. This shift has reoriented Russia’s global trade, making it heavily reliant on China and other Asian countries.

It is clear that Russia does not foresee agreement with the US and the West, making Asia, particularly China and India, its top priorities in economic and military cooperation.